“What is particularly curious is that in April 2026 Moldovan corn exports are not a continuous flow of goods at a more or less unified price, but a complex mosaic of routes, companies and product niches, each of which lives according to its own commercial logic,” notes Iurie Rija, an expert in agro-marketing.

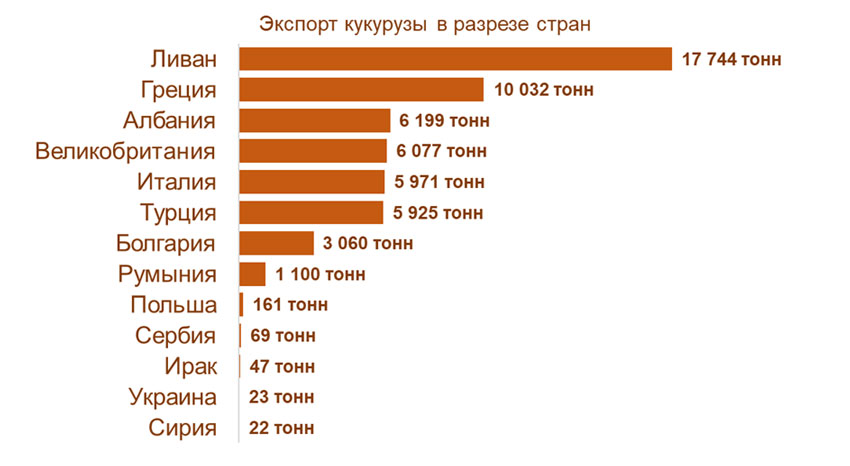

The geography of external supplies of corn from Moldova in April turned out to be very extensive – 13 countries, from the nearest neighbors to the Middle East and the British Isles. In this segment of the grain market last month there were 16 exporting companies with fundamentally different scales of activity and pricing strategies. The four largest operators accounted for about 95% of turnover, leaving the other market players with only “niche” exports – small in terms of tonnage (less than 5,000 tons in total), but with maximum price margins.

Exporters: vanguard and rearguard

On the first position of the leading four exporters is Orom-Imexpo SRL: – 9.5 thousand tons, 41.9 million lei (physical share of the April commodity flow – 16.8%, value – 18.3%). The average price of 4,426 lei/t was the highest among the four largest corn exporters.

The secret of success is simple: Orom-Imexpo SRL worked exclusively on the Lebanese and Albanian destinations, the two markets offering the best price conditions. In Lebanon, 6.6 thousand tons were shipped at the price of 4,628 lei per ton – the highest price among all three operators working on this route. To Albania – 2.9 thousand tons at 3,966 lei per ton. Orientation on two attractive (in terms of price) markets allows Orom-Imexpo SRL to outperform its competitors in terms of specific profitability.

Grando Invest Group SRL with the most concentrated strategy of external deliveries closes the four: one market – Great Britain, 6,1 thousand tons of goods at a single price – 3 443 lei/ton. The share by value (9.13%) is noticeably lower than the physical share (10.77%). Obviously, the company “bet on volume” and, perhaps, on the long-term contractual nature of relations with the British buyer. But, at the same time, some share of potential profit may have been sacrificed – for the sake of predictability.

Among the twelve second-tier companies, there are some notable choices. Prograin Organic SRL – supplying 207 tons of corn to Italy at a price of 4,658 lei/t. The name of the company speaks for itself: organic products that do not compete with mass products.

Another “niche player” is Lender Agroprim SRL: only 69 tons in total, but deliveries to two atypical (for grain trading in Moldova) destinations at once: Iraq (47 tons at 4,358 lei/t) and Syria (22 tons at 5,959 lei/t). Middle East diversification on a small scale is a potential growth point.

Conclusions

The market remains steadily Mediterranean-Middle Eastern, with Lebanon, Greece, Albania, Italy and Turkey together taking more than 81% of the total volume. And this concentration reflects not random demand, but established logistics chains with the Danube ports as a hub.

For exporters, this means high predictability of the main flow and at the same time dependence on the conjuncture of these very markets. Any increased competition from Ukrainian or Romanian grain on the same routes can seriously change price conditions already in the summer months.

Latent potential of niche destinations. Poland, Serbia and Ukraine together accepted less than 260 tons, but at prices in the range of 7,763-9,500 lei/ton. This is 1.9-2.3 times the average level. And this is a signal: where the mass operator does not go because of small volumes, the specialized company gets profit, which is unattainable on the main supply routes. For farmers considering the possibility of growing seed or organic corn, such figures are a strong argument in favor of investing in certification.

High concentration of corn exports from a corporate perspective. This is a sign of a mature market with high operational barriers to entry in a large segment. It is virtually impossible to enter the top segment in terms of production without its own infrastructure, a portfolio of long-term contracts, and access to working capital. That is why small companies intuitively go to a niche – there competition with Rusagro-Prim SRL or Agro-Nova Prim SRL makes no sense, but competition in terms of product quality is quite possible. The experience of Universal Agro SRL, which receives 9007 lei per ton, is the best proof of this.

Competition of “price strategies”. The April analysis in terms of “company × country” revealed a fundamental difference between two models: the “volume operator” operates in the range of 3200-4100 lei per ton; the “niche operator” – in the range of 7700-9500 lei per ton. To mix these strategies means to win neither.

Corn exports from the Republic of Moldova: distribution by country, April 2026. Source: Customs Service of the Republic of Moldova