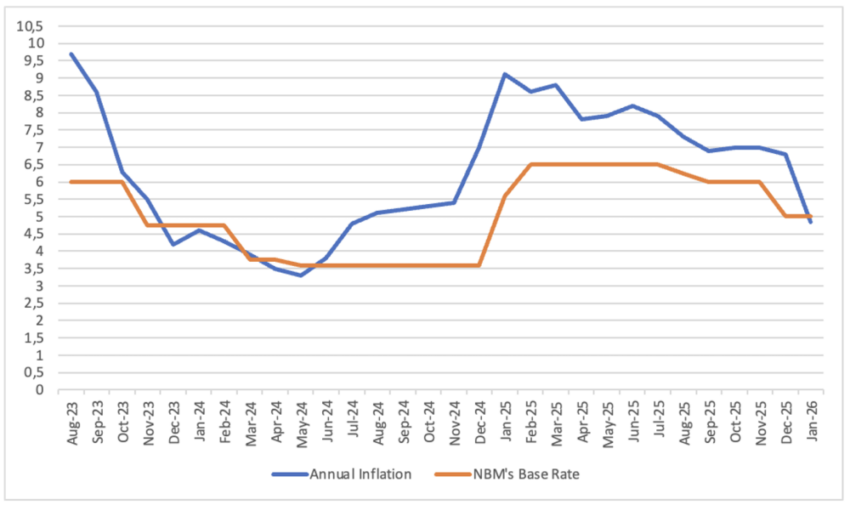

In December 2025, the National Bank of Moldova reduced the prime rate from 6% to 5% per annum, and in February 2026 confirmed this decision, keeping the rate at the same level. Obviously, the decision was approved in anticipation of the effect of earlier measures.

The National Bank resumed monetary policy easing measures back in August 2025, reducing the rate from 6.5% to 6.25% per annum. At that time, the regulator argued its decision by the fact that it was taken in the conditions of slowing annual inflation, and aimed at fixing inflation expectations, taking into account the time lags. But the decision in August was made in conditions when inflation had not yet entered the specified corridor – 5% per annum ±1.5 p.p. (i.e. in the range of 3.5%-6.5% per annum).

Inflation in August amounted to 7.3% per annum – still above the upper limit of the acceptable range (6.5%). Although the classical rule states that a prime rate cut stimulates inflationary pressure, the regulator continued its easing policy and cut the rate in September and December, and then maintained it in February.

In doing so, inflation behaved “out of line” and at the end of January 2026, it returned to the target band for the first time in 14 months, falling from 6.84% to 4.85% per annum. This is a very sharp decline in inflation: by 1.9 p.p. or by a third!

The dynamics of inflation over the past year deserves special attention. And since one of the most important instruments of the National Bank to maintain inflation in a given corridor is the prime rate, we have superimposed the dynamics of the two indicators in one graph.

Dynamics of inflation and the NBM reference rate (January 2025 – February 2026)

Taking into account the reality of what is happening, in its February decision, the National Bank did not further reduce the prime rate, keeping it at the level of 5% per annum. At the same time, it reduced the norms of mandatory reserve requirements for funds attracted by commercial banks in both lei and foreign currency by 2 p.p. and 3 p.p., respectively, to 18% and 26%. – To 18% and 26%, respectively. Such a measure, as the regulator emphasized, was aimed at covering the liquidity needs of the banking system and to support domestic demand.

This process started earlier. In 2024-2025, the NBM reduced mandatory reserve ratios for funds attracted by commercial banks in lei and in foreign currency. For lei, in April 2024 the norms amounted to 33%, which corresponded to 24.9 billion lei, but gradually the norms decreased and at the end of 2025 they amounted to 17.3 billion lei.

In foreign currency, the reserve norms were reduced from 43% in April 2024 to 39% at the end of 2025. The NBM indicates euro and dollar reserves separately: in April 2024 there were 258 million US dollars and 670 million euros in reserves; and 168 million US dollars and 469 million euros at the end of 2025.

Thus, by reducing the norms of mandatory reserve requirements for attracted funds through commercial banks, in less than two years, 7.6 billion lei (from deposits in lei) were released, as well as 90 million US dollars or 1.5 billion lei from deposits in US dollars and 201 million euros or 3.9 billion lei from deposits in euros. In total – 13 billion lei, which also put pressure on inflation.

Ideally, the funds freed from banks should be used to lend to the economy.

This has partially happened: if at the end of 2024 the volume of loans in the banking system amounted to 80.8 billion lei, at the end of 2025 – 103.6 billion lei. The growth for the year is 22.8 billion lei or 28.2%.

According to the volume of lending, it turns out that the loan portfolios of commercial banks “absorbed” part of the lei mass, which the National Bank “released” recently.

But the National Bank has another tool: currency interventions. And in 2025, the regulator actively sold euros: 190.5 million euros – the equivalent of about 3.7 billion lei.

NBM interventions in the foreign exchange market in 2025 (million euros)

|

Jan |

Feb | Mar | Apr | Mai | Jun | Jul | Aug | Sept | Oct | Nov |

Dec |

|

| SPOT operations | ||||||||||||

| BUYING | ||||||||||||

| Dolar S.U.A. | ||||||||||||

| Euro |

10,00 |

15,00 |

||||||||||

| SALE | ||||||||||||

| Dolar S.U.A. | ||||||||||||

| Euro |

22,40 |

25,50 | 1,50 | 1,50 | 27,60 | 64,00 | 40,00 |

33,00 |

Carrying out very serious interventions in the foreign exchange market, the National Bank for the first time in five years reduced the volume of its own foreign exchange reserves at the end of the year: they fell by 143 million euros in 2025.

Dynamics of the NBM foreign exchange reserves in 2020-2025 in mln *

|

USD |

EUR | USD |

EUR |

|

|

Absolute values |

Difference to previous year |

|||

| Dec 2020 |

3784 |

|||

| Dec 2021 |

3902 |

+118 |

||

| Dec 2022 |

4474 |

+572 |

||

| Dec 2023 |

5453 |

+979 |

||

| Dec 2024 |

5484 |

5247 |

+31 |

|

| Dec 2025 |

5104 |

-143 |

||

*Currency reserves until 2024 are shown in dollars, in December 2024 in both US dollars and euros, as Moldova switched to the calculation of the national currency to euros from the beginning of 2025.

But there are two more indicators to be taken into account: rates on government securities (GS) and the Moldovan leu exchange rate.

The rates on SS are kept at 9.0%-9.5% per annum (we are talking about the yield of indicative SS with the circulation term of 182 days or 364 days), and the freed funds of banks are placed also on this market. But these funds are not enough to cover the supply of the GS market. The Ministry of Finance may have problems with crediting on the GS market.

And the situation with the national currency rate is even more interesting. Recall that since January 2025, Moldova has switched to the euro as the base currency for setting the exchange rate. Since the introduction of the Moldovan leu into circulation on November 29, 1993, to calculate the exchange rate against other currencies, the leu was first determined against the U.S. dollar, and then, through cross rates – against other currencies.

From January 2, 2025, the euro became the pegging currency. Now, in order to understand whether the Moldovan leu is strengthening or depreciating, one should look at its exchange rate to the European currency, not to the American one.

Currency interventions of the National Bank, in particular, sale of currency, also release the lei mass and affect the Moldovan leu exchange rate. And foreign currency becomes attractive for commercial banks especially during the period of prime rate reduction.

In 2025, by selling foreign currency, the National Bank supported the leu exchange rate. For example, note in the table that in July, the NBM sold 64 million euros on the market, when the leu exchange rate reached at that time almost the maximum of 19.8376 (July 13).

This currency dump in July may have influenced the regulator’s decision in August to reduce the prime rate, which had been “stable” from February to July (6.5%). It also had to dampen demand for the euro in September and October.

But further support of the leu exchange rate is aggravated by the emerging negative dynamics of foreign exchange reserves. A reasonable question arises: to what amount of euro sales is the regulator ready to maintain the leu exchange rate in 2026, to the detriment of its foreign exchange reserves?

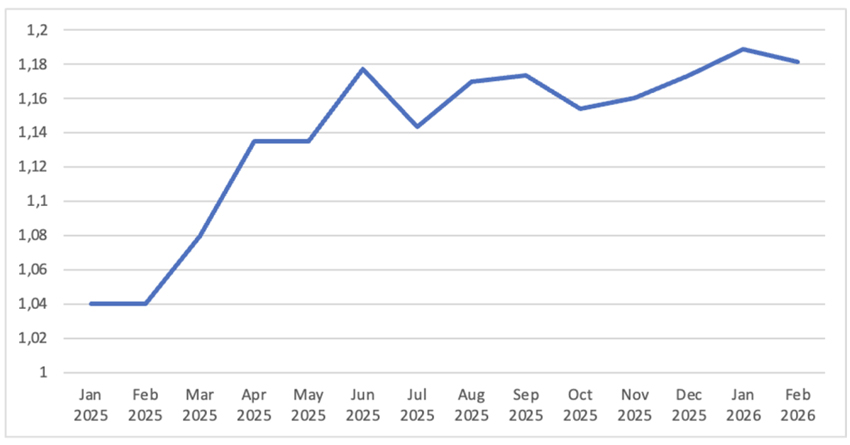

The situation is also complicated by a global factor: the Moldovan currency is a kind of “hostage” of the currency war between the euro and the U.S. dollar, which has intensified in recent months, when U.S. President Donald Trump spoke in favor of a weak dollar, thus stimulating exports.

As a result – the dollar is getting cheaper: if on January 4, 2025 the ratio of the US dollar to the euro was 1.03, by February 10, 2026 it will be 1.19.

Dynamics of the euro/US dollar exchange rate (January 2025 – February 2026)

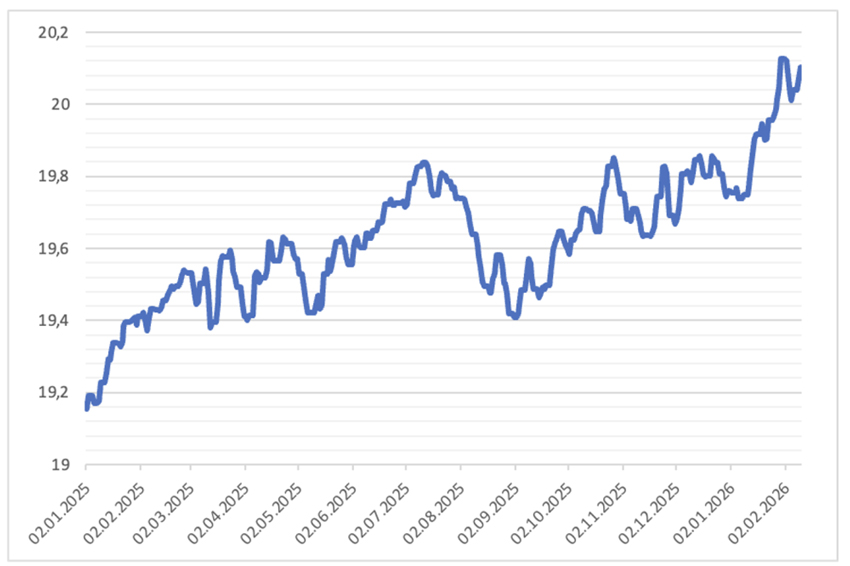

Therefore, there is nothing surprising in the fact that the Moldovan leu exchange rate in early February passed the mark of 20 lei per euro. Given the current trends, a return of the exchange rate below this level is unlikely in the short term.

Dynamics of Moldovan leu/euro exchange rate (January 2025 – February 2026)

It is still early to summarize the results, but some markers have already appeared. In 2025, the regulator was quite active in releasing the leu mass by several instruments at its disposal – through the interest rate, reserve requirements and currency interventions. A decrease in the prime rate, as a rule, leads to some depreciation of the leu. Reducing reserve requirement rates as well as selling currency also increases the leu in circulation. All this increases the pressure on inflation and the exchange rate of the national currency.

It is expected that these funds will be used to lend to the economy, as well as to meet the proposal of the Ministry of Finance to sell government securities. But with the expected decline in interest rates on government securities, the Ministry of Finance is unlikely to have enough bids to sell all the planned securities. (It should be recalled that in 2025, 9.1 billion lei from the sale of government securities were allocated to cover the budget deficit, while in 2026, the budget envisages a figure of 10 billion lei).

Finally, the leu’s peg to the euro will reflect the developments in the Eurozone, where the trend of strengthening of the euro against the US dollar is predicted by most experts and there are all grounds for this.

On the background of the mentioned events and facts, in Moldova, perhaps, we can expect a turnaround on some markets, which have been overestimated lately. Especially against the background of decreasing purchasing power of the population, which is a separate topic for discussion.

And, finally, it should also be mentioned: at the beginning of 2026, serious markers of the fact that the world is on the threshold of another crisis have appeared. In previous years, the echo of world crises reached Moldova a year later: the crisis of 1997 reached us in 1998, the crisis of 2008 reached us in 2009. But now, taking into account Moldova’s even greater attachment to the euro zone, the country will not have a “reserve” or “preparatory” year.

Shall we enter the crisis together with everyone else?

Commentary of InfoMarket agency